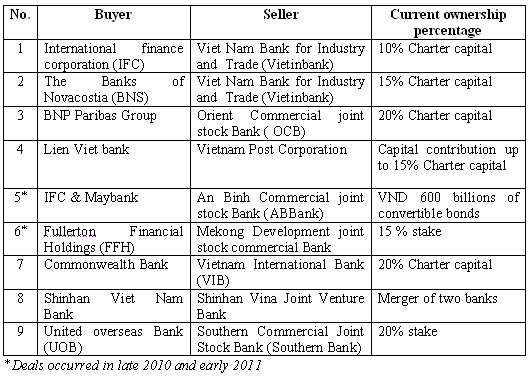

I. Overview of capital contribution and involved parties:

1. The license for the deal:

On February 21st 2011, the Prime Minister allowed VNPost to contribute capital to the LVB by the value of Vietnam Postal Savings Service Corporation (VPSC) and by cash and rename LVB to Lienviet Post bank (LPB). LVB receives intact VPSC. Vietnam Post and Telecommunication Group (VNPT) and VNPost implement the capital contribution in accordance with current regulations.

2. The involved parties:

LienViet Joint Stock Commercial Bank

LienViet Joint Stock Commercial Bank (LVB) was established and operated under the license No 91/GP-NHNN on 28/03/2008 of the Governor of State Bank of Vietnam (SBV). After 03 years, as of 28/03/2011, LVB has 50 deal offices and a total of 1382 staffs, charter capital of vnd 5,650 billion, total assets of vnd 40,000 billion, total accumulated profit of vnd 200 billion. LVB has attracted up to 50 thousand individual customers. The founding shareholders of LVB includes: Him Lam Joint Stock Corporation; Saigon Trading Group (SATRA) and Aviation Service Company, Southern Airports service Company (SASCO).

Vietnam Post Corporation

Vietnam Post Corporation (VNPost) was established under the Decision No. 674/QD-TTg on 01/6/2007 of the Prime Minister and officially went into operation on 01/01/2008. VNPost was set up to separate postal and telecommunication business of VNPT. VNPost has a network of 63 provincial postal offices, 07 subsidiary companies and nearly 18,000 service offices, including post offices, postal agents, kiosks and commune Postal cultural center in the whole country. VNPost is striving to become the leading corporation in supplying delivery service, financial and retail business in Vietnam.

Vietnam Postal Savings Service Corporation

Vietnam Postal Savings Service Corporation (VPSC) is a VNPost subsidiary, established under the Decision No. 337/1999/QD-TCCB on 05/24/1999 of the General Director of the General Post Office, which is now the Ministry of Information and Communication (MIC). VPSC’s charter capital is vnd 163 billion. VPSC’s business includes: Collect deposits, money transfer service, payment services among individuals who have savings accounts in postal savings system in Vietnam.

Before being transferred to the LVB, VPSC was a credit institution suffering losses. With a charter capital of vnd 163 billion and deposits collected up to vnd 5,380 billion, VPSC’s capital adequacy ratio was about 3%[1], much lower than 8% as regulated. In addition, VPSC had a loss up to vnd 145 billion. VPSC was insolvent because it borrowed money at 14% and lent at 12%. Therefore, VPSC was insolvent and might lead to bankruptcy.

3. The purpose of the involved parties

LienViet Joint Stock Commercial Bank

This capital contribution is an opportunity for LVB to develop the Postal Banking model with high potential growth in Vietnam, to expand the network nationwide, and to achieve the target that after 5 year of the merger, LVB will become 1 of 10 leading joint stock commercial banks and become the best retail selling bank in Vietnam.

Vietnam Post

The purpose of Vietnam Post is to get profit from the capital contribution by the value of VPSC which is higher than its book value, and to resolve the VPSC’s losses and its bankruptcy risk.

II. The results of the M&A deal

Following the capital contribution plan, all VPSC’s assets and liabilities will be transferred to the LVB. LVB will fully inherit all rights and obligations of VPSC. Therefore, all deposits in VPSC would be transferred to LVB, and VPSC could avoid bankruptcy.

VNPost, the state manager of VPSC will have vnd 360 billion in the form of equity contribution in the LVB. Thus, the recovery value for VNPost is enormous. VNPost not only avoided losing money but also got 4 times higher than the book value of VPSC at the time of the merger. According to capital contribution plan, VNPost will continue to contribute cash in LVB. In addition to investment purposes, this cash contribution is also effective in reducing difficulties in handling vnd 145 billion of VPSC’s current losses as well as other difficulties arising from receiving an in-danger institution.

LVB increased charter capital by vnd 360 billion (it will increase vnd 637 billion more in the future) and possessed the post office system which can be converted to banking transaction offices throughout the country. All of the rights of depositors in VPSC from now on will be protected as VPSC was allowed not to participate in deposit insurance scheme in the past, while LienViet-Post Bank is forced to participate in deposit insurance scheme.

In short, this deal can be considered as a resolution method in which LVB, as a healthy institution, agreed to purchase all assets and assume all liabilities of VPSC. The VNPost’s capital contribution to LVB has a great effect of preventing the bankruptcy of VPSC, ensuring the interests of depositors, as well as contributing to economic stability. In addition, VNPost, VPSC and LVB did not bear any major loss, but the three parties gained benefits and opportunities for new development. This deal is a typical case study of failed bank resolution with P&A method.

III. Challenges and opportunities to LienViet-Post Bank after M&A.

1. Difficulties and challenges

After the capital contribution, LienViet-Post Bank (LVPB) will face many difficulties and challenges as follows:

Firstly, the issue of management: LVPB oriented to the Postal Bank, a very new model in Vietnam. For successful development, LVPB should build a new management mechanism combining banking and post operation and successfully connect the two different credit systems.

Secondly, ensuring determined targets: According to the plan, at the beginning of 2011, LVB would pay dividends to shareholders at the yield of 15%. This is a challenge because after receiving the capital contribution by the value of VPSC, the total expenses of LVPB will increase and that might reduce profits in the next few years.

Thirdly, the issues of human resources: When the scope of business expands, management expenses, quality of staff are the issues for considerations. The Bank needs to recruit, train and retrain staffs in post offices to match with the banking standards.

Fourthly, upgrading infrastructure: To ensure uniformity of service quality, LVPB need to upgrade infrastructure at the post offices nationwide. This is a major challenge because there are a large number of post offices across the country.

Fifthly, the issue of IT integration: The integration of two different IT systems is always a difficult problem requiring a large investment in both hardware and software, training costs, and long time to carry out. In the current conditions, VPSC’s post offices spread across the country, many of them are in rural areas with communication difficulties and lack of equipment. These difficulties make it harder to integrate two different systems into an unified modern information system.

Sixthly, handling the losses of vnd 145 billion: When LVB receives VPSC, it is also responsible for handling the VPSC’s losses of vnd 145 billion. In addition, LVPB will also have to handle the potential losses from the low lending interest which is funded by high borrowing interest.

2. Advantages and opportunities

Besides the difficulties and challenges, LVPB also has many advantages and opportunities for development.

Firstly, the Postal Bank is a successful model in many countries around the world. LVPB is the first bank in Vietnam to follow this model. Through the capital contribution, LVPB can access to the system of post offices throughout the country. As the first postal bank and having the large post offices system to cover credit waves nationwide, LVPB has many advantages compared to other competitors. If the Postal banking model is successful, LVPB will become one of the largest and most important banks in the Vietnam banking system.

Secondly, the advantage of capital: The charter capital of LVPB has increased from vnd 5,650 billion to vnd 6,010 billion after VNPost contributed the value of VPSC to LVB. According to the capital contribution plan, VNPost will contribute a further vnd 637 billion in cash. Thus, the financial capacity of LienViet-Post Bank will be enhanced, that would help the bank to improve its competitiveness and develop a new business model.

Thirdly, the huge branches network: After the merger, LVPB will use nationwide post office network of VNPost to supply financial banking services. The development of LVPB’s networks is also less expensive and more convenient because there are many available good positions for banking business. With a very large number of post offices (11,000 points), which is over the transaction offices number of the Agribank, LVPB has favorable conditions for raising capital and providing products and services to people throughout the country, especially in remote areas where other banks have not reached yet.

Conclusion

The M&A deal between the VNPost and LVB has been successful so far because it has brought benefits for all three parties. The objective of Lienviet Postbank to soon become a leading bank in Vietnam with the postal-banking model is clear, but the path to achieve that goal isn’t simple because it depends on changing factors of financial and monetary markets. Under the aspect of failed bank resolution, the receivership of VPSC by LVB is a successful case of handling insolvent bank. This has great implication in directing and developing methods for problem credit institutions in order to best protect interests of depositors as well as ensure the stability of the banking system.

In the future, The LienViet – Post Bank’s objective achievements will depend on whether the bank can overcome challenges and take advantage of above mentioned opportunities. We look forward to the success in the future of this typical banking M&A deal in 2011.

[1] Estimated number (163/5380 = 3%)