DIV was established with special tasks on protecting legal rights and interests of depositors in Vietnam.

After the severe aftermaths of the Asia financial crisis that hit heavily regional financial system in 1997-1998, the nations in Asia found it necessary to make reforms and urgent needs to establish DI institution.

Although Vietnam was not directly influenced by the financial crisis, the poor economy background and inefficient state-owned enterprise system, for instance, the financial – banking industry in the country had made an incident in which a series of credit cooperatives came into failure in the period of 1980-1990, more banks confronted with difficulties and looked for financial assistance or even stopped operating. Public confidence on banking – financial system, in fact, had been heavily deteriorated.

These problems have put an urgent need to make reforms on economy and restore public full faith on banking – financial system. In this situation, the Government had policy on restructuring banking – financial system, termination of operation for unhealthy credit funds, and establishment of Deposit insurance agency in Vietnam in 1999 with objectives of protecting legal rights and interests of the depositors, contributing to stabilizing the insured organizations and consolidating banking activities.

Development stages:

The period 1999 – 2005

Since the first days of operation, DIV resolved successfully 31 credit funds that were failed prior to the establishment of DIV, made reimbursement for depositors of credit funds with total amount up to 14.3 billion VND, contributing to protecting depositors’ rights and interests and consolidating public confidence on banking activities. In this stage, DIV focused its targets on off-site supervision activities and on-site monitoring operation over people’s credit funds with total amount of up to nearly 1000 funds nation-wide; eventually giving prompt warnings to help the insured institutions make their shortcomings in operation, ensure stability of credit funds and safety of banking system.

The period of 2005 up to present

The year 2005 was considered an important transitional milestone of DIV development. The legal framework for DI activities had been consolidated by the Decree 109/2005/NĐ-CP dated 24 August 2005 in which object of insured depositors had been expanded; coverage had been increased to protect depositors in the best manner, consolidating the reaffirmed position of DIV in the national financial safety system.

GD of DIV Mr. Bui Khac Son (third from the left) participated in the International Conference on DI in Indonesia

The year 2005 is the period of time in which, Vietnam economy in general and the banking – financial system in particular, had achieved impressive progresses in growth. Flexible but prudent monetary policy of the SBV has brought into play the efficiency, contributing to reducing pressures on inflation, stabilizing monetary market, and creating favorable environment for banking activities.

In front of renovation requirements for development purposes, DIV set to work immediately to research on building and implementing the project “restructuring DI system, building centered- customer organizational model. Monitoring, supervision had been moved from compliance to compulsory risk-based model, gradually researching to apply international modern standards (like CAMELS) combined with experimental reality in Vietnam. The quality of monitoring and supervision activities are eventually improved, contributing to effective control of commercial banks through potential risk warnings system and legal compliance in banking operation and DI policy implementation, pushing up consolidation and enhancement of effectiveness of activities of credit funds.

Especially, prompt payment of deposits is an important factor in increasing public confidence on DI agency in particular and the entire banking system in general. As of 30 June 2009, DIV has implemented payment of DI for depositors in 36 people’s credit funds with total amount of nearly 19 billion VND, contributing to consolidating and enhancing trust of depositors on banking – financial system.

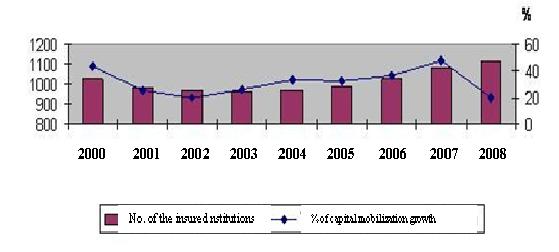

Together with strong development of banking – financial system with target of average capital mobilization growth to reach about 30%/year over the past years, an increasing number of the insured organizations has been seen, affirming public trust on banking – financial system (Graph 1).

Graph 1: The number of the insured organizations and the whole system capital mobilization growth in the period of 2000 – 2008 (Source: DIV)

This result re-affirmed DIV has contributed to the efficiency of politic-economic stability, giving positive influence to capital mobilization capacity of credit funds.

Current challenges, vision and expectations:

International settings

Since 2008, the world has been facing the global financial crisis with bank failure happening daily in the US and many countries throughout the world. In such conditions, the role of DI Institution is highly appreciated in a joint effort together with the Government, Central bank to overcome crisis. In America, Federal Deposit Insurance Corporation (FDIC) has received and resolved, on and for behalf of the US Government, 78 failed banks since 2008. DI agency in the world has implemented many positive measures such as receivership and resolution of problematic financial institutions, an increase in DI payment coverage, or commitment on blanket coverage in a bid for enhancing public trust.

International exhibition on banking – financial – deposit:

Domestic settings

With the dynamic and in-depth integrated economy, this financial crisis has heavily and directly hit the Vietnam economy such as a decreasing GDP, export turn-over reduction, and dropping foreign investment capital drop. In that situation, the Government has proposed many measures to prevent downturn in banking – financial sector.

For DIS, the process of reform, integration of banking – financial system, on one hand, creates opportunities for development, but on the other hand, sends big systematic challenges: i) fund maintenance, ii) operation and market risk management in the process of systematic restructure; and iii) public awareness enhancement on DI.

Vision and expectation

In front of the present challenges, on basis of lessons to be withdrawn in various countries in the term of crisis resolution, DIV has pro-actively built its development strategy by 2012 and the vision up to 2020 with focusing the target on becoming a modern financial institution, meeting international standards on operation and a pillar in the national financial safety net, contributing to pushing up healthy and stable development of banking system in a line with market principles.

The development orientation of DIV on basis of risk-minimizer model inclusive of 5 important pillars: i) Construction of legal infrastructure; ii) Consolidation of financial capacities and systematic transparency maintenance; iii) Diversified development and improvement of services & products quality and international integration; iv) Restructuring, HR development and management capacity enhancement; and v) IT-based modernization of DI activities.

The five sustainable development pillars of DIV shall be implemented in a synchronous and effective manner in the framework of the project “Financial Sector Modernization and Information Management System” (FSMIMS) funded by the World Bank to support the SBV, CIC and DIV. The project has total investment of nearly 80 millions USD and duration of 6 years up to 2014.

10-year development for a new model of insurance is not considered a long time as it is necessary to meet conditions that are required and sufficient to realize into social life. But the whole 10 year is connected with 2 cycles of international and regional economy development that was fallen into crisis, nations are aware of the necessity to have an effective DI in order to get the unhealthy economy out of crisis in a fast and cost-effective way for tax-payers. This awareness is derived from the lessons learned from the experimental crisis that is called the most dangerous and hardest to resolve like a crisis of public confidence. No countries, even of strong financial capacities and the most developed banking system, can confront with the problem in which people are loosing trust on institution and pushing up the event of the run on bank. People’s faith is built on basis of the government’s commitment on ensuring the safety of every single penny of savings deposits of the insured organization depositors, and that once the insured organizations are forced to close, depositors shall receive their deposits in the most prompt way, of both principle and interests without loosing any cents. If seeing to it in this point-view, over the past 10 years, DIV has completed successfully their tasks. Thousand of depositors in the credit funds that are closed, are paid fast and correctly. The statistics report shows that credit funds can mobilize better on basis of credit of depositors on the DI system. These achievements of DIV are attained thanks to the strategic view, continuous supports of the Government since the decision on establishing DIV in 1999, comparing with the neighboring situations in which many countries have DI agency established for only 1-2 years or even under preparation process. These remarkable progresses are achievements of 20 years for renovation and integration of the Vietnamese economy – not only meaning a dynamic development but a sustainable development.