According to the International Association of Deposit Insurers (IADI)’s guidance on the coverage limit, the limit should synchronize with the 2 main objectives of deposit insurance policy, which are typically to protect small and unsophisticated depositors and to contribute to financial stability. Setting the coverage limit should ensure 2 principles: firstly, the limit should be high enough to maintain depositors’ confidence in banking systems; secondly, at the same time, the limit should be low enough in order that large depositors are not careless with banks' unsafe and risky activities, thereby, minimizing moral hazards, avoiding excessive risk-taking in

In setting the coverage limit of a particular country, the following factors are usually considered: i) GDP per capita, inflation, foreign exchange rate, public confidence in the financial and banking system…; ii) the ratio of fully covered depositors to total eligible depositors; iii) the ratio of fully covered deposits to total eligible deposits; and iv) risk levels of the banking system and the economy as the whole.

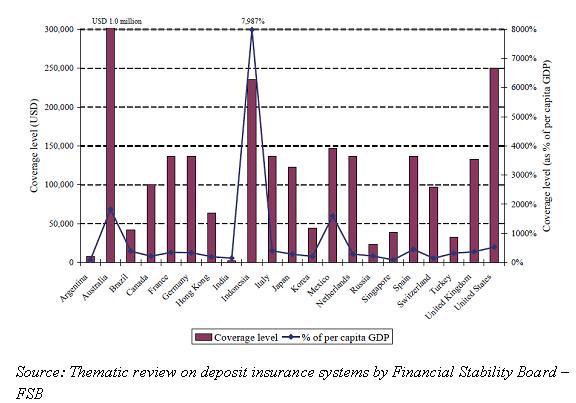

1. Setting coverage limits during normal period of time

Countries often set the coverage limit 2.5 -5 times GDP per capita, covering about 80% of depositors and about 30% of total eligible deposits during periods when their economy grows stably.

According to the survey by Financial Stability Board (FSB), as shown in the below figure, for those countries where data are available, an average of 84% of total eligible depositors was fully covered, with the highest being Brazil (98.9%) and the lowest being Italy (55%). The FDIC (United States) covers deposits up to $250,000. At that level, 99.7% (almost full coverage) of the number of depositors are fully covered. EU’s limit covers 98% of depositors. In terms of value of deposits fully covered as a percentage of total deposits, nineteen countries provided figures with an average of 42%, with the highest being the United States (79%) and the figure of EU being 60% .

Coverage limits in some countries

Besides, experience shows that inflation, changes in components and sizes of deposits may have negative effects on coverage limits, leaving them unsuited to public policy. Therefore, it is necessary to adjust the coverage limit periodically. In those countries with stable economic growth, low inflation and sound financial system, the adjustment is more predictable and less frequent than in others with less developed financial system and the economy undergoing instability. For example, in United States, FDIC is mandated to reconsider the coverage limit every 5 years. Meanwhile, in Zimbabuwe where high inflation is prevalent, the coverage limit is reviewed every 2-3 years. According to IADI, in 2012, some deposit insurers have increased the coverage limit such as Australia, Thailand, Peru, Trinidad&Tobago and Ukcraina.

Adjusting coverage limit during the financial crisis

Adjusting coverage limit is an indispensable component of the package of measures taken against the negative movements of financial system during the global financial crisis. During the crisis, public confidence in general and depositors’ confidence in particular were adversely affected, therefore, raising coverage limit or adopting a blanket guarantee system to better safeguard depositors, reassure them, thereby, minimizing “bank runs”.

As per statistics provided by IMF and IADI, 48 countries introduced new policies, measures including coverage limit adjustment. Of which, 19 adopted blanket protection, 23 raised the insurance limit permenantly while 6 others announced a temporary increase in insurance coverage.

During the crisis, Asian countries maintained a high protection equivalent to 5-80 times GDP per capita. In South East Asia, most countries increased the coverage limit or adopt blanket protection. After the crisis, countries unwound blanket guarantee and shifted back to limited coverage. However, most countries have kept the coverage limit higher than in pre-crisis period ever since.

Coverage limits in some countries in pre and post-crisis periods

|

Country |

Pre-adjusted limit (USD) |

Post-adjusted limit (USD) |

Compared with GPD (times) |

Fully covered depositors/total depositors (%) |

Fully covered deposit/total deposits (%) |

|---|---|---|---|---|---|

|

U.S |

100,000 |

250,000 |

5.4 |

99 |

79 |

|

Taiwan |

49,965 |

Blanket guarantee from 10/2008 to 12/2010 then adjusted to 99,930 |

4.96 |

98.6 |

59 |

|

Thailand |

- |

Blanket guarantee during the crisis then adjusted to 31,960 USD from 11/8/2012 |

5.92 |

- |

- |

|

Indonesia |

11,111 |

222,222 |

79.9 |

99 |

61 |

|

Philipines |

5.750 |

11500 |

6 |

99 |

- |

|

Malaysia |

19,468 |

Blanket guarantee and adjusted to 81,428 USD |

8.4 |

99 |

- |

|

Russia |

13,000 |

23,000 |

2.5 |

96 |

31 |

|

Brazil |

35,800 |

48,000 |

6 |

98 |

21 |

3. Some recommendations for Vietnam

- Increasing the current coverage limit of 50 million VNN to be suited to the related factors: i) high GDP growth rates leaving the current limit equivalent to only 1.8 times GDP per capita; ii) high inflation and strong fluctuations in exchange rate making real value of the limit considerably low; value of deposits and number of depositors rising many times over years and; iv) complex changes occurring in the economy and in the financial system. The coverage limit should be in the range of 2.5 – 5 times GDP per capita, fully cover about 80% of eligible depositors and about 30% of eligible deposits in order to comply with international practice. Adjusting the limit up to an enough high level will maintain public confidence, thereby contributing to create favorable conditions for the Government implementing reforms and restructuring the banking industry in particular and the economy as the whole in general.

- Shifting to the blanket guarantee system when a financial crisis occurs. The shift can immediately stop bank runs. However, this mechanism may increase moral hazard and cause difficulties to transition to the limited coverage system afterward. Therefore, blanket protection should be adopted cautiously and only in case the worst scenario happens. At the same time, an exit plan for the transition to limited protection in normal time should be drawn up, in which, timeframe for the transition should be specified considering factors such as: possible impacts on public confidence, possibility of meeting public policy’s targets and a post-crisis suitable coverage limit.