Exchange rates have fluctuated in allowed stable band

Eventhe recent interest rates rise by Fed was not beyond markets’ expectations, there were doubts if the exchange rates in Vietnam would be increased. However, improved foreign exchange reserves and abundant supply of foreign currencies… were considered by experts as reasons for stable exchange rates, not as concerned. That was right but not enough, because that stability wasrootedin theactive management of the State Bank of Vietnam (SBV), most clearly reflected by the application ofcentral exchange rate regime over the past 2 years.

The experts also acknowledged that it was easier for a central bank to regulate its domestic currency than foreign currenciesbecause uncontrollable factors of foreign markets may have impacts on the foreign exchange rates. That was also the reason for the fact that under the USD pegged exchange rate regime, when facing external impacts, the SBV’s intervention in foreign exchange market was often rather passive causing unexpected shocks to market participants.

Although the regulation by the SBV was highly appreciated during that time, deeper global integration along with people’s higher expectation and sensitivity and the USD pegged exchange rate regime inadvertently restricted the regulators and made themso passive. Then the new regime of central exchange rates was born of that backdrop, coming into effect in January 2016.

Up to now, the central rate regime has been applied for nearly 2 years helping to stabilize foreign exchange rates in Vietnam despite the fluctuations of the global economy and financial system. The most important thing is that the psychologyof over-expectation and even speculation in foreign exchange trading has been eased much since the exchange rates have been stabilized for recent years, especially thanks to the new exchange rate regime.

Besides, other evidencesuch as rapidly increasing numbers of foreign visitors to Vietnam and foreign investment amount (both direct and indirect)…partly shows foreigners’ confidence in Vietnam’s stable macro-economy and the fact that the worries about exchange rate fluctuations have been eliminated. The balance of payment, foreign exchange reserves, money supply control…have then been improved over recent years. This also explains why although the Fed has continuously signaled their rates hikes, lately on 13th last December, the exchange rates in Vietnam market have remained“unruffled”.

Being more active, flexible and ready

That does not mean the foreign exchange market would be stable by itself without the intervention of regulators as recently suggested by some specialists to applya regime called “floating foreign exchange rates”. This could be learnt from painful experiences of our neighboring countries in the region.

“Many low income and developing countries are applying the floating foreign exchange rates regime. Some other economies in transition also tend to apply more flexible framework of foreign exchange rates. However various experiences prove that even developing countries need certain management of foreign exchange rates. The rationale is that the regulation would ease the impact that foreign exchange rates may have on the economy in case of abrupt shocks, said Ms Ha Thi Kim Nga, an economic specialist from the International Monetary Fund (IMF) in Vietnam.

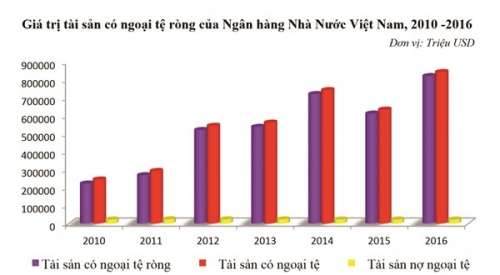

Central exchange rates regime contributes to improving the net foreign assets of the State Bank of Vietnam. Source: IFS

As mentioned above,it is easier for a central bank to regulate the domestic currency than foreign currencies because of not only objective external factors in context of Vietnam’s global integration but also internal factors. Foreign exchange rates are always sensitive due to its vulnerability to not only economic events but also people’s expectation and psychology.Dollarization has been strongly mitigated through recent years but still exists. Therefore if the problem of people’s over-expectation is not solved, dollarization may come back strong.

As cited by an SBV high-ranking officer, historical statistics show that there were cases where the supply of foreign currencies exceeded the demand but due to people’s over-expectation and speculation, the SBV still had to sell more foreign currencies for meeting the demand. In contrast, there were cases such as in 2014 when happened the occurrence of 981 drilling rig, the market turned very tense, but thanks to good communication, the market soon came back stable and the SBV did not have to sell foreign currencies. Those examples illustrate huge impact of people’s over-expectation and psychology on foreign exchange rates.

According to Ms. Nga, the proper role of and regulation mechanism for foreign exchange rates are not easy to be determined and in fact, this is a challenge for every country as there is no one-size-fits-all approachto finding an appropriate rate regime for its relevance to other economic factors, for instance, open or closed capital account, the extent of dollarization…

In Vietnam, eventhough there has not been any out-of-control problems arising from the application of the central exchange rates regime but we should be aware that: Vietnam remains a small economy and Vietnamese dong is still a non-convertible currency. Therefore, an active and flexible intervention of the SBV is still in need, besides the central rate regime which has been facilitating the exchange rates to respond to signals of both domestic and external markets.

One of the factors ensuring the active intervention is sufficient foreign exchange reserves. Some experts assert that with the current foreign exchange reserves of more than USD 46 billion, the regulators are totally capable of intervening in and regulating the market if necessary. However, the SBV should continuously increase the foreign exchange reserves to improve the capability of regulating exchange rates, realizing objectives of monetary policy, making international payments, especially to prepare a efficient buffer to cope with big external shocks caused by foreign markets in future.