In fact, there exists no universally approved definition of the CSR of a corporation. Still, as observed in our shared knowledge at the moment, CSR is perceived to be the entire responsibility of an enterprise for the impact on society from its decisions and business operations. From this, we could see that CSR is only achieved when enterprises have a sense of respect for the law as well as all the commitments with its stakeholders; (when businesses) associate their business activities with its role in resolving social and moral issues, environmental protection, human rights protection and response to customers’ concern; and prevent and minimize possible negative impacts of businesses’ activities on society.

An organization with a high CSR in its ethics shall always be fully aware of the effects of its operations on society and the environment, and also has the correct evaluation and responsibility for those actions. This implies organizations’ transparent and ethical behavior will contribute to the sustainable and steady development of the whole society, especially to the social welfare and health issue. In addition to the economic benefits, enterprises' CSR also has a direct impact on people (i.e., social issues such as living and working environment, civil rights, etc...), the planet (environmental safety), and sustainable and steady development.

The Deposit Insurance of Vietnam (DIV) is established as a state-owned financial institution in order to perform the deposit insurance profession, with the mandate to: “Protect depositors’ legitimate rights and interests, contribute to the stability of credit institutions, ensure the safe and sound development of the banking system.” That objective constitutes the mission that the DIV needs to shoulder. Thus, it can be seen that DIV’s missions have already contained its CSR, and such missions require the DIV to fulfill them with a high sense of responsibility and, above all, the duty to protect insured depositors.

The fundamental task of the DIV is to protect the legitimate rights and interests of depositors, who are the individuals having deposits in Vietnam Dong at insured institutions. These depositors have the right to be reimbursed with the full amount of their deposits within the coverage limit as prescribed by law. The depositors' legitimate rights and interests have been fully recognized, respected and protected by the law through professional activities of the DIV - a specialized agency established by the Government to carry out direct social responsibility with depositors. At a higher level, DIV's activities which come out as the results of the spreading effect are also the representation of its CSR to the whole society and are also the act of fulfillment of DIV's political mission.

The DIV performs reimbursement to insured depositors in insured institutions in accordance with the provisions of legal documents, with the highest in the hierarchy is the Law on Deposit Insurance No 06/2012/QH 13 (18/06/2012), the following lower-ranked document is the Decree No 68/2013/NĐ-CP (28/6/2013) explaining in details and guiding the implementation of the Law on Deposit Insurance and Circular No 24/2014/TT-NHNN (06/9/2014) providing some guidance in deposit insurance activities; the last is the Statute on Payment of Insured Deposits issued by the Board of Directors of the DIV and the Guiding Document for Payment of Insured Deposits, issued by the General Director of the DIV. This documental system provided the detailed, clear and transparent regulation /announcements/instructions about all rights and interests of insured depositors and stakeholders; the procedures of reimbursements to depositors are carried out clearly, starting with a comprehensive public announcement on the mass media (Clause 3, Article 26 of the Law on Deposit Insurance): Time of reimbursement, its location, reimbursement method(s), list of insured depositors eligible for reimbursement. This is also conformant with the recommendation in Principle 17 of the Core Principles for Effective Banking Supervision of the Basel Committee on Banking Supervision (BCBS) and the International Association of Deposit Insurers (IADI): “The deposit insurance system needs to give depositors prompt access to their insured deposits. Therefore, the deposit insurer needs to notify or provide sufficient information in advance in cases where reimbursement is required and have early access to depositor information. Depositors have a legal right to receive reimbursement within the coverage limit and must be informed of the time and the conditions under which the deposit insurer initiates the reimbursement process, the timeframe for payment, whether it is prepayment or emergency payment, as well as the corresponding coverage limit”.

In recent years, the coverage limit of insured deposits has changed positively. On October 20, 2021, the Government issued Decision No. 32/2021/QD-TTg stipulating the coverage limit for reimbursement made by the deposit insurer for insured depositors. Accordingly, from December 12, 2021, the coverage limit (including principal and interest) per depositor at an insured institution has increased to 125 million VND, netting a growth of 50 million VND compared to the previous limit of 75 million VND. This demonstrates the needed focus of the Government and the State Bank in protecting the practical interests of the majority of depositors at insured institutions. This also shows the interest in the social responsibilities in the policies and advocacies of the Government.

The fact that the DIV always has respect for the law and fully fulfills its commitments to stakeholders in its reimbursement activities, with stakeholders are insured institutions and depositors in those institutions, has played an important role in stabilizing depositors’ mentality and contributed to maintain the social order when there is any problem at those insured institutions. Reimbursement helps depositors have more financial resources to sustain their living or invest to improve their household finance. That is undoubtedly the implementation of DIV's CSR through its reimbursement activities, which helps promote the association of a deposit insurance profession with the solution of social and moral issues, furthers the protection of depositors' legitimate rights and interests; and thereby successfully responds to the everyday concerns of all stakeholders.

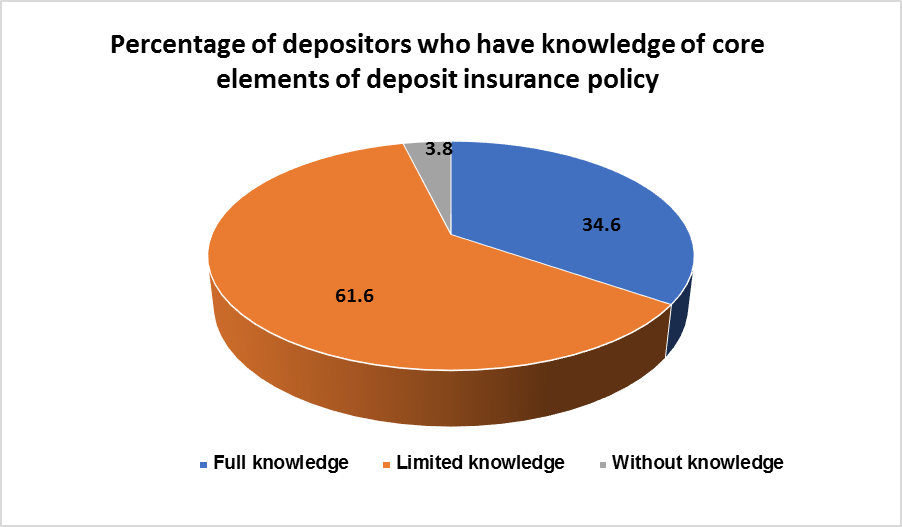

On the other hand, during the reimbursement process, the DIV has also integrated communication activities on deposit insurance when dealing with specific cases of every depositor to help the public have more knowledge and information about the deposit insurance activity, the rights and interests of depositors; and DIV's and insured institutions' responsibilities. As a result, depositors could have careful considerations about choosing insured institutions with good performance to entrust their deposits.

The intertwining of professional activities with the dissemination of knowledge to depositors is also the method that the Philippine Deposit Insurance Corporation (PDIC) uses with regard to this country's depositors. Currently, PDIC is the IADI organization with the most transparent and decisive message on deposit insurance systems' CSR. As early as 2009, PDIC launched a nationwide campaign named "Be a Wise Saver" (BAWS). The core purpose of this campaign is to disseminate basic knowledge about savings, banking operations and measures to protect the deposits of vulnerable groups in society such as students, retirees, small businesses, and the disadvantaged. This program is a PDIC's valuable CSR-imbued success. Afterward, in September 2020, PDIC released an official statement about its CSR: “PDIC will make all efforts to help all Filipinos have a considerable financial literacy level.” The message clearly shows the impression of CSR on PDIC's operations: PDIC will communicate the basic financial knowledge to the people and help them have a better understanding about the topic, the basis from which they can make better saving decisions and know how to choose and access appropriate banking and financial services.

From the viewpoint of the World Business Council for Sustainable Development (WBCSD), businesses need to be responsible to the society, expressed through responsible and ethical commitments/conduct and helpful contributions to economic development in order to improve the social material-mental welfare. DIV's operations in general and the reimbursement processes, in particular, cannot be divergent from the standards of the era and the world.

DIV's activities have made immeasurable socio-economic contributions when the DIV connects and harmonizes professional activities to fulfill social responsibilities (Business for Social Responsibility - BSR). This can be considered a complete success of the DIV, a success achieved in a way that respects the ethical values and fundamental rights of depositors as well as the community and the natural environment.

Research and International Cooperation Department

References:

http://www.pdic.gov.ph/csr_literacy_activities

https://ndic.gov.ng/resources/corporate-social-responsibility/